What is the Effective Annual Interest Rate?

The Effective Annual Interest Rate (EAR) is the interest rate that is adjusted for compounding over a given period. Simply put, the effective annual interest rate is the rate of interest that an investor can earn (or pay) in a year after taking into consideration compounding.

EAR can be used to evaluate interest payable on a loan or any debt or to assess earnings from an investment, such as a guaranteed investment certificate (GIC) or savings account.

The effective annual interest rate is also known as the effective interest rate (EIR), annual equivalent rate (AER), or effective rate. Compare it to the Annual Percentage Rate (APR) which is based on simple interest.

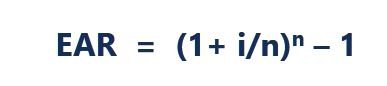

The EAR formula is given below:

Where:

- i = Stated annual interest rate

- n = Number of compounding periods

How to calculate the EAR

Calculating the EAR can provide you with a benchmark rate you can use to compare the interest rate of one loan to that of similar loans, allowing you to make more informed financial decisions. To calculate the effective annual interest rate, follow these four steps:

1. Determine the number of compounding periods

When calculating EAR, it’s useful to first consider how often interest compounds. Your EAR is likely to be higher if compounding happens more times per year. If you compound it monthly instead of annually, the EAR becomes much greater than the nominal rate, or the interest rate before adjusting for inflation. Compounding might occur annually, monthly, quarterly or even daily.

2. Find the periodic rate

Once you determine the number of compounding periods, you can calculate the periodic rate, which is the annual interest rate divided by the number of compounding periods in a given year. For example, if you borrow $100 from the bank and plan to pay back that amount over the next 12 months at an annual percentage rate of 6%, the periodic rate would be 0.5%. You can use the following formula to calculate this rate:

Periodic rate = Annual interest rate / Number of compounding periods

3. Use the EAR formula

To obtain the EAR, add one to the periodic rate and multiply it by a figure that’s equal to the number of periods per year. You can then subtract one from your previous result and multiply it as a percentage to obtain the EAR. The following formula represents the EAR, where “r” represents the nominal rate and “n” represents the number of compounding periods per year:

Effective annual rate = [(1 + r) / n]^n – 1

4. Check your results

After obtaining the EAR, it can be beneficial to review your result to ensure you’ve calculated it correctly. You can then use the EAR to compare loan offers or different savings accounts. Remember that as the number of compounding periods increases, the EAR also increases. Understanding compounding can make it easier to make an informed choice about which loan or investment may be best for you.

Benefits of calculating the EAR

Here are some of the primary benefits of calculating the EAR:

It makes it easier to compare investments

The EAR offers a precise way to measure interest earned over time. This calculation can help investors better understand how a certain interest rate might affect their investments and bottom line. EAR valuations can also make it easier to choose between different investment options, such as certificates or bonds versus cash or savings accounts.

If you’re considering an investment with a higher interest rate than your current investment, it can be beneficial to use the EAR to determine whether the additional yield is advantageous. The more frequently your money earns interest, the more valuable it becomes over time since more of its earnings compound each year. When comparing two similar investments where one pays monthly and another pays quarterly, you can use EAR to determine which option has more value over time.

It can be useful for comparing loans

When comparing two loans, you can use the EAR to determine the actual annual interest rate for both. This calculation can help you choose a cheaper loan with the most favorable repayment plan. The ability to compare two loans accurately can make it easier to determine which loan you can afford.

For example, if you plan to borrow $10,000 at an annual interest rate of 10% and make six payments per year, your EAR for that loan would be 10.38%. This means you’d pay $1,038.30 per year in interest on a $10,000 loan. If you applied for another $10,000 loan with a rate of 10% but only made one payment per year, you’d only pay $1,000 per year as interest for the loan, making it more affordable than the first.

It can provide increased accuracy

The EAR accounts for compounding over a given period, meaning it can provide increased accuracy, especially compared to the annual percentage rate or the nominal interest rates. Knowing how to calculate the EAR can help you make more informed financial decisions and allow you to obtain higher rates of return if you’re depositing and lower ones if you’re borrowing. When borrowing a loan, being able to calculate the EAR can make it easier to know what to expect when you receive your monthly billing statements.

Limitations of the EAR

The EAR can be useful for making more informed financial decisions, but there are a few important limitations of this calculation to consider:

-

It doesn’t consider other fees or charges associated with a loan. While the EAR can provide a useful way to compare two loans, the calculation doesn’t incorporate the additional fees that loans often contain. For example, if one loan offers a lower rate but charges origination fees and another offers a higher rate but doesn’t charge any fees, the second loan may be less expensive, even if their EARs are similar.

-

It doesn’t account for any prepayments on your loan. If you pay off all your capital early on a loan, the EAR calculation may appear as if you’re paying less than what you’re supposed to be paying throughout the year. Accounting for prepayments can provide you with an even more accurate estimation of how affordable a loan might be.

-

It isn’t typically the standard for banks. Banks and other financial institutions typically use the stated interest rate or the annual interest rate in the original contract when advertising loans, rather than the EAR. This is because the stated interest rate tends to be lower than the EAR, so if you want a more accurate estimation of the interest rate, it may be necessary for you to calculate the EAR yourself.

What is compound interest?

Compound interest is calculated on the initial principal and also includes all of the accumulated interest from previous periods on a loan or deposit. The number of compounding periods makes a significant difference when calculating compound interest.

The Bottom Line

Banks and other financial institutions typically advertise their money market rates using the nominal interest rate, which does not take fees or compounding into account. The effective annual interest rate does take compounding into account and results in a higher rate than the nominal. The more the periods of compounding involved, the higher the ultimate effective interest rate will be.

The higher the effective annual interest rate is, the better it is for savers/investors, but worse for borrowers. When comparing interest rates on a deposit or a loan, consumers should pay attention to the effective annual interest rate and not the headline-grabbing nominal interest rate.

-

{kind=link}