Banks may not have been the earliest adopters of the cloud, but industry leaders now realize that a cloud-based digital strategy enables a range of strategic advantages—including improved sustainability.

Cloud adoption rates are accelerating as all financial institutions strive to move more deftly, launch products more quickly, and hone operational efficiency. This was confirmed in a report late last year from the Economist Intelligence Unit (EIU). For instance, U.S. fintech Varo Bank claims that with the cloud driving its digital services it can operate 75% more cheaply than a traditional bank. These benefits are then passed on to the end customer by way of lower-cost, tech-led banking services.

Crucially, the move to the cloud is now as pronounced among Tier 1 and Tier 2 banks as it is among industry disruptors. Last year saw a flurry of deals. HSBC committed to using Amazon Web Services to develop new digital products and support security and compliance standards, while Wells Fargo signed on Google and Microsoft as public cloud providers. Google has agreed similar partnerships with Deutsche Bank and Goldman Sachs. PayPal, meanwhile, used a cloud-based software-as-a-service (SaaS) deployment model to roll out its new Buy Now, Pay Later (BNPL) proposition across four major markets, citing it as “the fastest start to any product [it has] ever launched.”

How green banks work

Clean energy development in the US is typically funded by production and investment tax credits, which — as the name suggests — encourage companies to either invest in wind, solar, and other clean technology or to produce more clean energy in exchange for reducing their taxes.

Green banks work much more like a regular bank — lending money for clean energy or energy-efficiency projects with an expected return on investment. Green banks essentially use a combination of public and private money, taking a smaller amount of public funds and leveraging private dollars to grow projects.

Green banks are set up in a variety of ways. The New York Green Bank is a division of the New York State Energy Research and Development Authority. Michigan’s green bank is a nonprofit. Connecticut’s is quasi-public, created by a bipartisan state legislature bill in 2011. Australia’s green bank — the largest in the world — is owned by the government. Still others like California’s are part of state infrastructure banks, which fund local infrastructure projects like roads, bridges, schools, and municipal buildings as well as clean energy development

“[In Connecticut,] we’re an intermediary between the policy objectives of the state and the private markets,” Connecticut Green Bank president and CEO Bryan Garcia told me in an interview. “We use private-sector discipline to achieve public sector goals.”

Since it was started in the mid-aughts, the Connecticut Green Bank has ushered in $1.94 billion worth of investment into the state’s economy. The vast majority has been from private investment, a full $1.65 billion — and for every dollar of Connecticut Green Bank investment, the state is able to attract $6.60 of private investment in projects. It’s estimated that this has not only reduced energy cost savings for over 55,000 families and close to 400 businesses in the state, but it’s also resulted in the installation of 434 megawatts worth of clean energy.

One state over, New York Green Bank founder Richard Kauffman’s experiences managing the loan portfolio in Barack Obama’s Department of Energy shaped what he wanted to do — and not do — for a green bank at the state level. One thing Kauffman wanted to avoid was giving out government subsidies for projects that might have happened without help from the government. He instead wanted the bank to find projects that were struggling to attract private money, the kind that could really benefit from a green bank loan.

“You want to think about a green bank as being a double incubator,” Kauffman said. “It can both incubate financing structures and also demonstrate that by scaling up a loan product, it can become financially attractive for the private sector.”

In other words, Kauffman saw green banks as an opportunity to invest in smaller projects that private banks might otherwise overlook and grow them to the point where the banks and credit unions actually wanted to get involved. One of New York’s Green Bank funded community solar projects that allowed people to buy a stake in a community project. People who either couldn’t afford solar panels or couldn’t find space for them on their roofs still were able to subscribe to community solar and reap the benefits of cheaper electricity.

The Connecticut Green Bank has also done a lot of work on solar projects, especially gearing its programs toward lower-income communities and residents who might not otherwise be able to get panels installed.

Intelligent Finance

This is at the heart of the recent strategy shift from Huawei’s Enterprise Business Group Financial Services Industry group which we saw in Singapore this week at the Intelligent Finance Summit. We heard from Huawei leadership Ryan Ding (President of Enterprise BG) and Jason Cao (CEO Global Digital Finance), as well as industry notables such as author Dave Birch, DBS CIO Jimmy Ng, and Vincent Loy from the MAS; all debating the challenges and opportunities in the intelligent, digitized remake of the financial services industry that we’ve seen which rapidly accelerate during the pandemic.

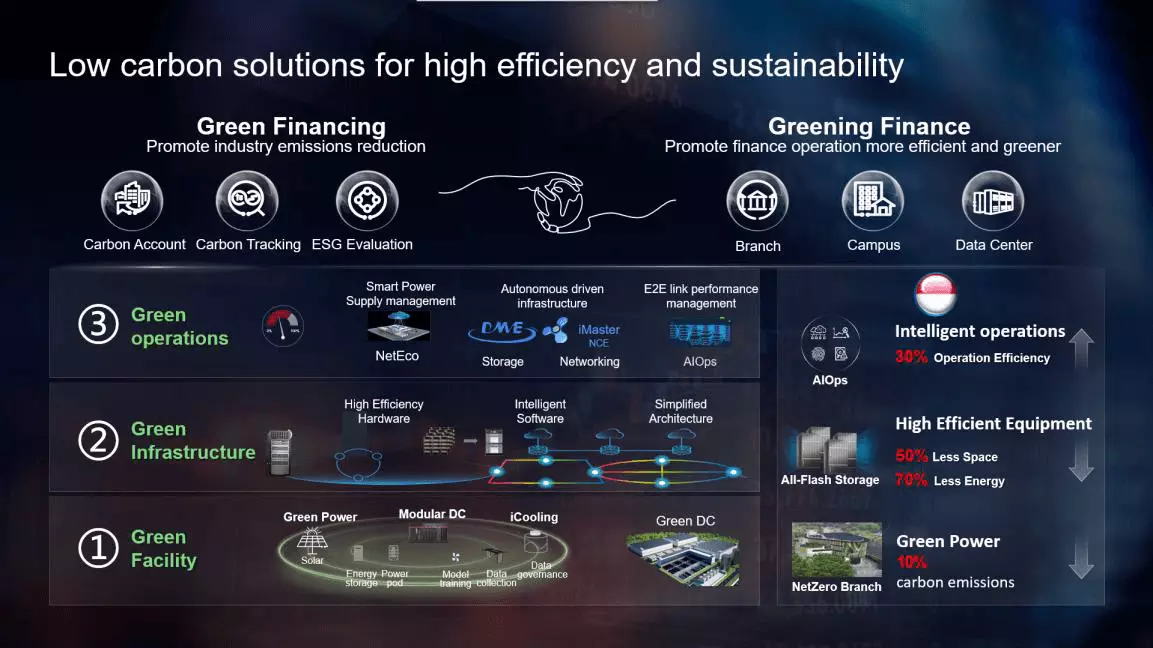

A theme that emerged early is the work Huawei has done on creating a specialist cloud architecture for financial services, and the key to this development is an unyielding focus on energy-efficient operation. As both Ryan and Jason contended, the digitilization of financial services creates a big energy consumption problem for the world. Banks are already big users of energy, as seen by the statistics above, but digital transformation efforts are pushing that energy consumption to dangerous new heights when seen in the context of rising global temperature and eco-distress.

China as the Proving Ground for the FSI Cloud

Huawei is now the largest provider of financial services cloud capability in China and is the fastest growing of the top 5 cloud providers globally. But to illustrate the size of the problem in China, Huawei shared some mind-blowing statistics. Energy consumption is directly correlated with compute power and data consumption, so a market the size of China is always going to be a critical proving ground for more energy-efficient operations.

China Merchants Bank, for example, has a 10 Petabyte (Pb) data volume annually. ICBC, the largest bank in China, has already offloaded 90% of its mainframe traffic to the cloud, meaning its cloud stack is utilized 12 Billion times per day. China’s postal savings bank has a 600m active user base. On top of this, as we see AI implementation, data utilization is intensifying. The metaverse will also generate more demand for cloud-based services, with the Bank of “Things” and metaverse platforms combining to create the equivalent of 75 Billion digital humans by 2030 alone (Source: Huawei EBG)

Sustainable, Green Infrastructure must be Autonomous and Cloud Based (Source: Huawei EBG)

As Cao detailed, in recent years as demand for their cloud operations has exploded, Huawei has invested heavily in autonomy, power management, and generation. Focusing on renewable power sources such as solar, more effective data center energy management, and energy recycling.

Fortunately, we have digital energy or digital solutions for energy consumption, and we have [solar] PV energies as well as smart energy. The second aspect we’re focusing on is power consumption. For banks to use a lot of equipment, we can actually apply technology to improve the efficiency of heat spreading so that the power used for the cooling system will be reduced. And specifically we have designed some recycle system for heat to be dispersed efficiently and smartly.

A Smart World Needs Sustainable Compute Power

Between 1956 and 2015 the world saw a 1 Trillion-fold increase in computing power. To illustrate, the 1985 Cray-2 supercomputer was surpassed by the iPhone 4 release in 2010. Our modern smartphones have millions of times the processing power, storage capacity and memory of iconic computers like the Apollo Guidance Computer that took the Apollo astronauts to the moon. But as we move into an era of autonomous supply chains, smart cities and artificial intelligence, the computing demands will just intensify by orders of magnitudes. Becoming smart 21st century economies will require a ton of energy, but as we fight climate change simultaneously, we’ll need to revolutionize energy management of our combined computing infrastructure.

All of this autonomous capability will have massive benefits to society in terms of operational efficiency and massive cost reductions, lowering the cost of basic services like healthcare for example. As an illustration of this, DBS Bank in Singapore shared that the cost-to-income ratio of their digital segment was less than half that of their traditional operations historically. In my recent book, we estimate we could cut the total cost of US healthcare by 70% using a range of technologies by the mid-2030s, mainly around AI.

The Metaverse

To round out our discussion though, I wanted to change tack a little and jump into the Web 3, crypto + metaverse world. The task of breaking down this at the Summit future space fell to my good friend Dave Birch. Dave gave a 15-minute masterclass on why the Metaverse matters and how crypto, NFTs, CBDCs, and tokens fit into our near-term future.

Dave broke down the Metaverse hype into three core components — the virtual worlds we will interact with (Augmented worlds overlaid on our real-world and immersive virtual worlds), the tokenized digital assets we’ll own or utilize, and our credentials and identity we’ll use in those digital worlds.

When we hear talk about the Metaverse and Web 3, the focus is often on the nature of the digital worlds themselves and what we’ll do there, the virtual property we’ll own, and the role our avatars will play. But as Dave Birch explained, in the metaverse we’ll need to be uniquely identified and we’ll need to transact, just like in e-commerce and m-commerce applications today. But it will need to be much more seamless and interactive than the way we pay for things today, hence leading to the inevitable capabilities of our wallets. Our wallets are moving into the cloud because they have to — you can’t use cash or swipe a card in the metaverse, nor in the 21st century smart economies emerging tomorrow.

The future of the world is digital, and if we’re going to make it sustainable and green, we need to make a massive investment in energy-efficient cloud operations. Likely this means that most of our day-to-day banking will move out of on-premise core systems to the cloud. The size of investment in hardware and intelligent cloud architecture to make this happen is massive. Everything relies on this though. Not only our presence in the metaverse but every real-time, contextual, embedded finance and banking scenario of the future.

{kind=link}